A Political Risk Wave On Top Of Economic Risks

Parliament's seat distribution that came out of the June 7 general election opened a door that could carry Turkey from authoritarianism to democratization, but it also brought about a series of political uncertainties.

Parliament's seat distribution that came out of the June 7 general election opened a door that could carry Turkey from authoritarianism to democratization, but it also brought about a series of political uncertainties. The political scene has now become an equation with multiple variables.

After 13 years of single-party rule, Turkey now faces a coalition government. But which parties are going to form this coalition, whether it will be a long-term government, or whether it will bring political stability is not yet known. It may take months for a government to be formed and to obtain vote of confidence from parliament, so actors in economy are very concerned - particularly about the option of an early election.

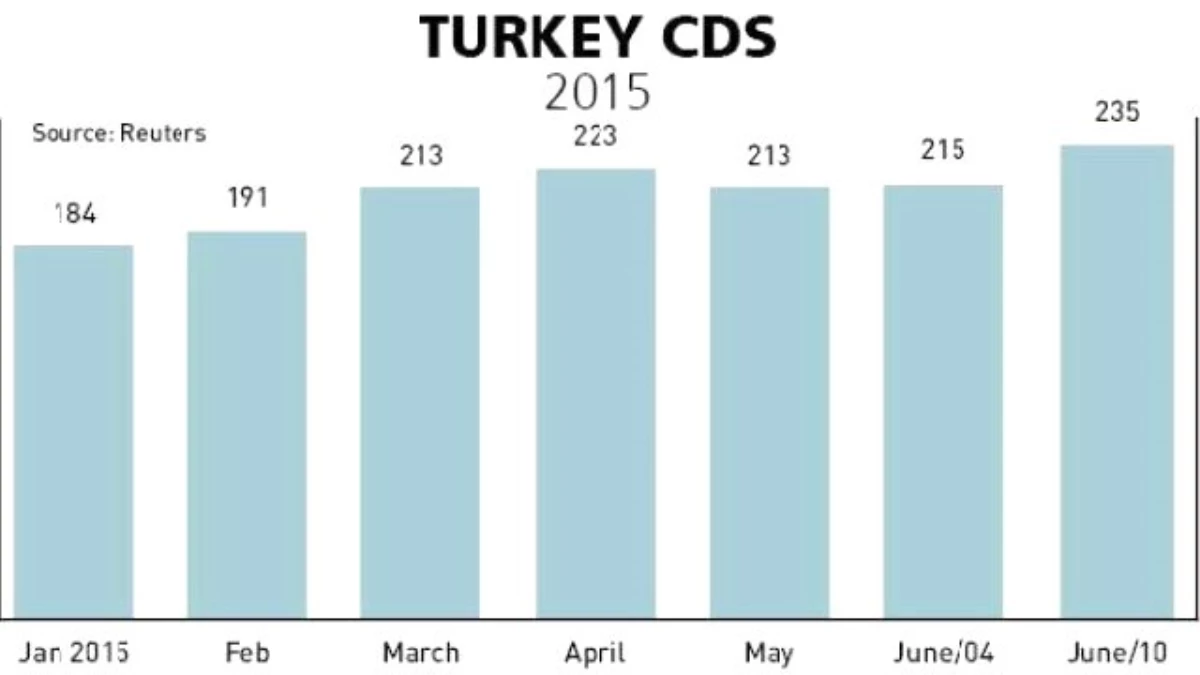

Credit development swaps

Such political uncertainties face Turkey at a time when its risk premium has climbed to the top, along with Russia and Brazil.

If you have invested in state bonds of a country and you want to insure you investment, insurers have a price for this risk according to the country's situation: Credit development swaps (CDS). By looking at a country's CDS you can understand how risky it is at certain times.

Two days prior to the election, Turkey's CDS was 215. This was the third highest among emerging countries. At the top was Russia with 332 and Brazil was second with 240. South Africa and Indonesia came after Turkey. These countries are named the "fragile five."

The course of the CDS from the beginning of 2015 shows that Russia has recovered relatively but Brazil and Turkey have rising CDSs with their increasing risks. The risk premiums of South Africa and Indonesia show a moderate increase.

These five fragile countries are named as such because their commitments and debts are far beyond their assets. The risks they carry are not only economic but also political and geopolitical. Russia's premiums climbed amid the tension with Ukraine and the Crimea crisis, and it was also affected by low oil prices. In January 2015, Russia's risk premium reached 573 and the Russian ruble devaluated considerably. Even though Russia has since recovered relatively, it is still the most risky emerging country.

Brazil's risks stem mostly from its economic situation. The country, which experiences balance of payment troubles, is also faced with a threat to domestic stability because of the wide income distribution gap.

Increase in CDS after elections

While Turkey's CDS was 215 on June 4, it increased 20 points to 235 after the election on June 7 - a 9 percent climb. This actually means approaching Brazil in second place and maybe surpassing Brazil soon.

Turkey's risks are economic, political and geopolitical. Turkey's foreign debt is $403 billion, which corresponds to 53 percent of its national income, while the debts due within just 12 months amount to 40 percent of the total. Turkey is hugely affected by the U.S. Federal Reserve's interest rate increases. It also cannot attract as much foreign capital as it previously did. So it is trying to meet its deficits by using reserves and indefinite sources.

What's more, the Turkish Lira has lost more than 30 percent of its value against the dollar over the past year, increasing its vulnerability.

Turkey's risk premium (CDS) minimized in 2010, after peaking in the economic crisis year of 2008. It has now started climbing again.

Dollar/Turkish Lira

At the beginning of the weak following the election, the Turkish Lira was 2.80 against the dollar, the lowest level throughout its history. The Istanbul Stock Exchange also plunged 6 percent. The euro/Turkish Lira climbed to a record-breaking high of 3.10, while the currency basket also hit a record with 2.96.

The devaluation of the lira against the dollar since the beginning of 2015 has reached 21 percent. Over the past 12 months, the lira has lost 33 percent of its value against the dollar.

Zero growth in industry and investment

The IMF recently revised its growth expectation for Turkey in 2015 from 3.4 percent to 3.1 percent. However, on June 10, Turkey's surprising first quarter growth data was released, showing that gross domestic product (GDP) increased 2.3 percent compared to the first quarter of 2014. The prediction of economists responding to Bloomberg's survey had been 1.7 percent. This means growth beyond expectations, but annual growth reaching 3 percent depends on the performance of subsequent quarters.

In the first quarter, Turkey has shrunk nearly 3 percent in terms of dollars.

Personal consumption expenditures were determinant in the growth beyond expectations. Household consumption increased 4.5 percent in the first quarter, while public consumption expenditures rose 2.5 percent. On the other hand, investments did not increase at all compared to the first quarter of the previous year, not contributing to growth. While public investments rose by over 10 percent, private sector investment increased by almost 2 percent. Net exports did not contribute to growth.

It was the service sector that pioneered first quarter growth. Growth in services was 4.1 percent, while growth in the finance sector was also noteworthy.

On the other hand, growth in agriculture was 2.7 percent while it was very low in industry and negative in construction. Growth in industry remained at 0.8 percent, while in the mining sector there was shrinkage of 8 percent. Manufacturing, which has a share in GDP of more than 25 percent, grew 0.8 percent in the first quarter.

The construction sector, which has lost its tempo considerably, shrank 3.5 percent compared to the first quarter of 2014.

Fitch says tensions aggravated

Turkey's economy is able to grow with foreign capital inflows, and when foreign investment withdraws it stagnates and may even enter a crisis. What will happen to the foreign capital inflow, which was already weak in 2014, in the coming months? How are foreigners evaluating the risks in the new political terrain?

Evaluating the outcome of the election, international rating agency Fitch Ratings said it "increases near-term political uncertainty."

The results of the June 7 elections "may aggravate tensions regarding economic policy," which "could increase risk to the sovereign credit profile" it added. "Economic policy coherence and credibility in Turkey has been weaker than in rating peers."

Fitch also stated that a coalition might bring "moderating influences" into play, but this is far from certain. "Conversely, increased political uncertainty, the possibility of another election and heightened market pressure on the exchange rate may put the Central Bank to the test, aggravate existing tensions and increase the risk of erratic policymaking or the pressure for looser fiscal policy, ultimately leading to widening budget deficits" it said.

In short, extended uncertainty in politics comes at the same time as the U.S. moves to tighten its monetary policy. If this situation causes major shifts in the perception of foreign investors, of which Turkey has an extraordinary need, then the economic destruction may be higher than expected and cost inflation may be added to all, increasing discontent.

(Graph) - Istanbul